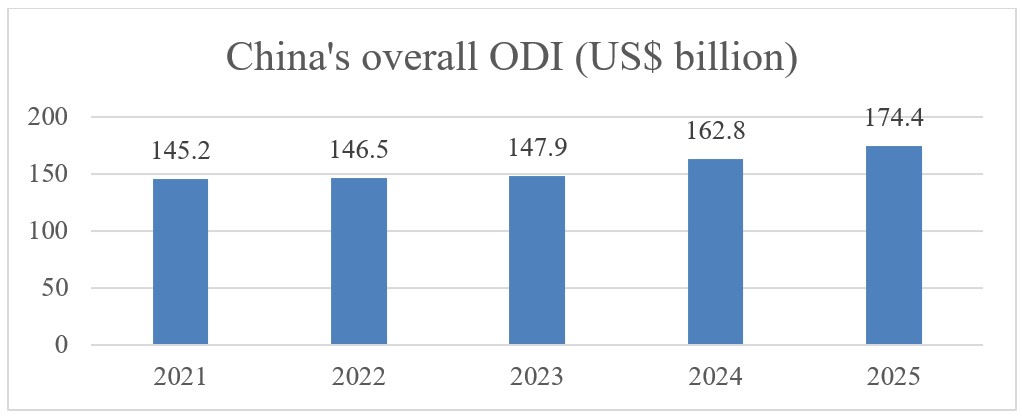

Figure: China’s overall ODI (US$ billion)

Sources: Statistics published by MOFCOM of China

China’s ODI regime has historically been governed by a filing and approval framework administered primarily by the National Development and Reform Commission (NDRC), the Ministry of Commerce (MOFCOM) and foreign exchange authorities. With Chinese investors now operating over 50,000 overseas enterprises across approximately 190 countries and regions—and with investment trends shifting from traditional infrastructure toward high-tech manufacturing, EV supply chains and green energy—regulatory focus has increasingly turned to national security considerations. In this context, the Regulations introduce a more security-driven comprehensive framework governing outbound investment activities by Chinese investors. The framework integrates export control restrictions into outbound investment activity. Projects involving Chinese investors, financing or technical participation—particularly those in the AI, robotics, and critical minerals space—will require more intensive diligence and ongoing monitoring.

Key Features of the Regulations

The Regulations largely preserve China’s existing ODI framework while introducing several important developments:

-

Broad Scope of Application (Articles 2 and 33): The Regulations apply to all Chinese investors, including enterprises, other organizations and individual residents. Outbound investment is broadly defined to include direct or indirect acquisition of ownership, control, management rights or other interests in overseas businesses or assets, including through contributing assets or equity or by providing financing or guarantees. Article 33 further clarifies the scope of the framework by confirming that overseas financial market investments (using an investor's own, raised or entrusted funds) and offshore reinvestments are subject to the Regulations and other applicable rules. Taken together, Articles 2 and 33 bring resident individuals within the State Council-level outbound investment framework and provide a basis for future rules governing their outbound investments. Key issues, including the treatment of existing offshore holdings and any applicable filing, reporting, threshold or exemption requirements, remain subject to further rulemaking.

-

Enhanced Export Control and Data Compliance Requirements (Articles 13–14): The Regulations further integrate ODI regulations with China’s export control, technology export, cross-border service and data governance regimes.

Article 13 prohibits unauthorized exports of restricted goods, technologies, services and data and explicitly covers indirect transfers through overseas personnel assignments, technical support and training activities. Accordingly, investors may not transfer any restricted technical know-how services or related data that are subject to export control, including through the organization of personnel to work abroad.

Article 14 confirms that outbound investments remain subject to a wide range of regulatory requirements, including foreign exchange, export control, cybersecurity, cross-border data transfer, merger control and state-owned asset supervision rules.

-

Outbound Investment Security Review (Article 15): Article 15 provides a State Council-level legal basis for an outbound investment security review mechanism. Relevant authorities, including the NDRC and MOFCOM, may review outbound investments and may extend to certain transfers or disposals of overseas assets and interests associated with outbound investments that affect or may affect national security. While detailed procedures and filing thresholds are yet to be clarified, this development elevates national security from a factor considered within ODI approvals to a standalone regulatory regime. Conceptually, the mechanism shares certain features with recent outbound investment screening regimes adopted in other jurisdictions, including aspects of the U.S. outbound investment review framework, although important differences and implementation details remain to be clarified; consequently, U.S.-China cross-border transactions could be subject to parallel review processes.

-

Investor Protection and Countermeasures (Articles 19–25): The Regulations strengthen protections for Chinese investors abroad through enhanced government services, international cooperation and consular assistance. More importantly, the Regulations establish a broad legal basis for China to adopt countermeasures against foreign governments, organizations or individuals that impose discriminatory restrictions on Chinese investors or China’s interests. Such countermeasures could include restrictions on import and export activities related to China, investment in China or transactions with Chinese organizations or individuals.

-

Overseas Litigation, Investigations and Data Production (Article 22): The Regulations also address the provision of information and evidence in connection with overseas disputes and investigations. Chinese organizations and individuals involved in outbound investment-related litigation, arbitration, regulatory investigations or enforcement proceedings must comply with Chinese laws governing state secrets, data security, personal information protection, export controls, technology export administration and judicial assistance when providing information or materials overseas. Where Chinese law requires governmental approval before information may be provided abroad, the relevant approval procedures must be completed.

-

Strengthened Enforcement (Articles 27–29): The Regulations significantly strengthen ODI enforcement. Violations may result in confiscation of illegal gains, fines ranging from 0.1% to 1% of the investment amount, forced divestiture and restrictions on future outbound investments for up to three years. The Regulations also introduce express monetary penalties for directly responsible personnel.

Key Considerations for Businesses

- Adopt a Holistic Compliance Approach. The Regulations make clear that ODI compliance is no longer limited to obtaining approvals or completing filings. Companies should assess, at an early stage, whether a transaction may trigger export control, technology export, cross-border data transfer or national security review requirements. The Regulations may have implications beyond Chinese investors themselves. Foreign counterparties, joint venture partners and acquisition targets may increasingly encounter Chinese outbound investment, export control and data compliance conditions as part of transaction execution and post-closing operations.

- Revisit Existing Investments. Investors should review existing outbound investment projects for potential compliance gaps, particularly where ODI filings, foreign exchange registrations, reporting obligations or post-investment changes may not have been fully implemented.

- Embed Regulatory Conditions into Transaction Documents. For acquisitions, joint ventures, greenfield investments and other outbound transactions, companies should consider making key regulatory approvals, filings and compliance requirements conditions precedent to closing, rather than addressing them post-signing or post-completion.

- Heightened Scrutiny in Sensitive Sectors (including AI, Robotics and Critical Minerals). Companies operating in the AI, robotics and lithium battery materials sectors are particularly exposed to these developments. Regulatory scrutiny over outbound transfers of technology, intellectual property and talent is expected to intensify and companies headquartered outside China may face exposure through their counterparties in cross-border partnerships or technology sharing. Accordingly, companies in these sectors should exercise heightened caution, particularly given that the Regulations provide a clear legal basis for authorities to require the unwinding of completed overseas transactions.

- Prepare for Increased Transaction Complexity. The Regulations may affect not only Chinese investors but also overseas companies, investment funds, real estate developers, financial institutions and other counterparties receiving Chinese capital. Chinese investors may require additional information regarding a green field investment’s or a target company’s business operations, technology, data practices, ownership structure, customer base, supply chain relationships and post-closing operations in order to complete their own regulatory analysis. Depending on the circumstances, Chinese regulatory approvals, export control assessments, data compliance reviews or security review considerations may become conditions to closing. In transactions involving sensitive technologies, data-intensive businesses, critical infrastructure, energy assets, strategic resources or national security considerations, Chinese regulatory developments may directly affect transaction timing, diligence requirements, long-stop dates, cooperation covenants and overall deal certainty. As a result, counterparties should factor potential regulatory delays and execution risks into transaction planning, negotiations and timelines from the outset.

In summary, the Regulations mark the beginning of a new phase in China’s outbound investment regime. For both Chinese investors and their global counterparties, the early involvement of cross-border transactional and regulatory counsel, together with thorough preparation and proactive compliance planning, will be increasingly important.