Alert

A Moving Target: Tax-Qualified Plans and Other Employee Benefits

The House and Senate propose changes to the tax rules governing retirement plans and other employee benefits.

Alert

By

Takeaways

11.17.17

Tax reform, including changes to retirement plans, health and welfare plans, and fringe benefits, is well underway as the House and Senate move forward with legislative efforts. On November 16, 2017, the House passed its tax reform bill, the Tax Cuts and Jobs Act. The Senate proposal released on November 9, 2017 was revised on November 14, 2017 and approved by the Senate Finance Committee late on November 16, 2017.

Background

On November 2, 2017, the House of Representatives introduced its long-rumored “Tax Cuts and Jobs Act.” The House Ways and Means Committee approved various amendments to the bill on November 9, 2017 and sent the revised bill to the full House for a vote. The House passed the revised bill on November 16, 2017 (the “House Bill”).

Also on November 9, 2017, the Senate Finance Committee released its proposal for a tax reform bill, “Description of the Chairman’s Mark of the ‘Tax Cuts and Jobs Act.’” The Chairman’s mark was significantly modified on November 14, 2017 and was approved with minor additional modifications by the Senate Finance Committee on November 16, 2017 (collectively referred to as the “Senate Proposal”). As of the date of this alert, the Senate Finance Committee has not released a proposed tax bill.

If enacted as they currently stand, both the House Bill and the Senate Proposal would make certain minor changes to retirement plan benefits and would eliminate the favorable tax treatment of many treasured fringe benefits. Employer-sponsored health and welfare plan benefits would be left largely untouched. The House Bill and Senate Proposal are expected to evolve as they progress through the legislative process.

Proposed Laws

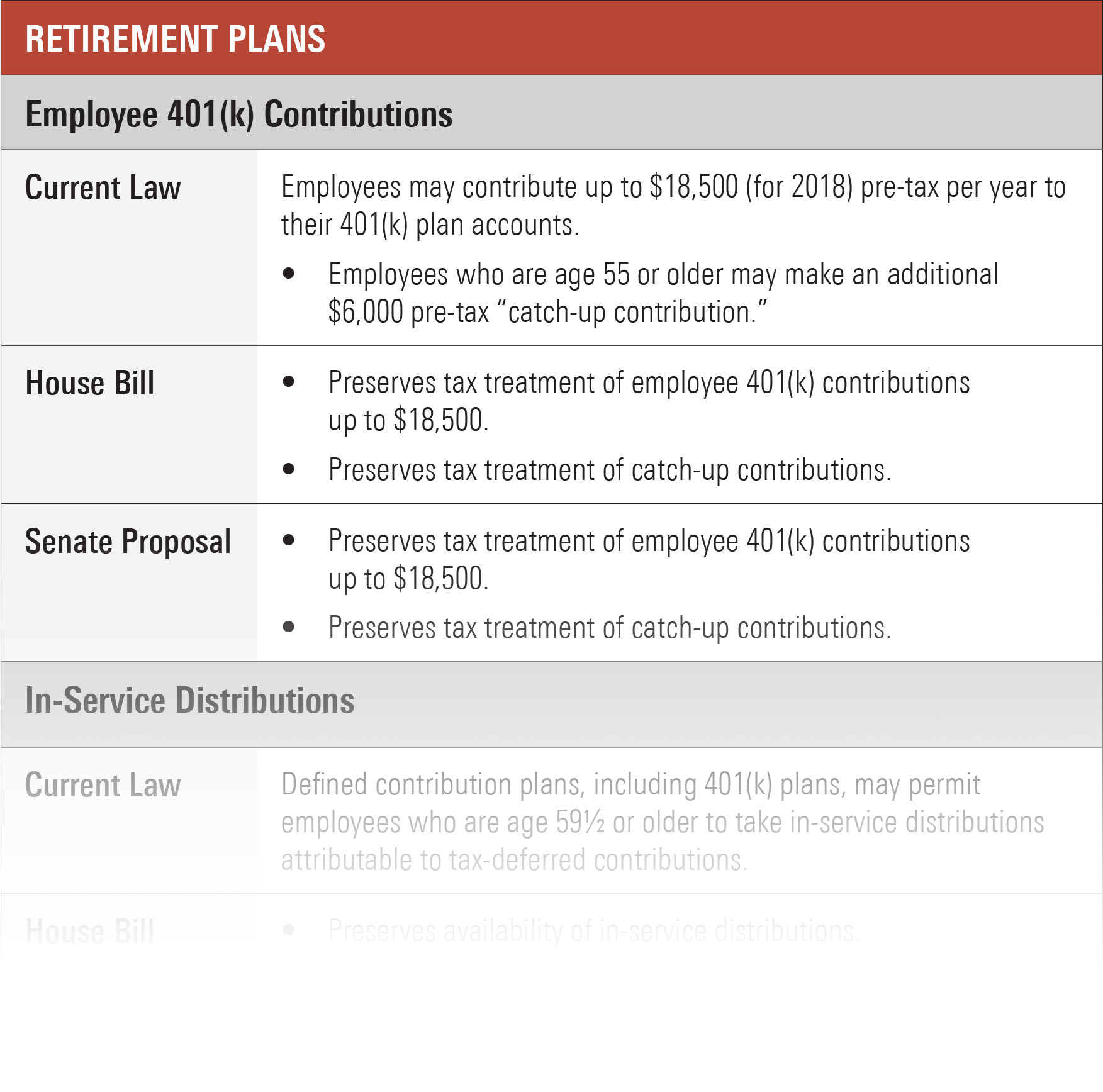

The table below summarizes the key retirement plan, health and welfare plan, fringe benefit, and employment tax provisions of the House Bill and the Senate Proposal.

Click here to view the full table (pdf).

Although the nature of these changes is unsettled, employers should begin to prepare for impending change by taking the following steps:

- Communicate the possibility of these changes to your employees during the open enrollment process. For example, indicate in open enrollment materials that all tax-favored benefits are subject to change based on pending tax reform legislation.

- Review the definition of “compensation” in your qualified retirement plans. Many employers currently include fringe benefits that are taxable to employees as “compensation.” The proposed changes would cause many fringe benefits that were previously not taxable to become taxable. If employers do not amend their plans to exclude specific sources of taxable compensation, they may be required to make increased employer contributions to their qualified retirement plans based on the newly includable sources of compensation.

- If you have employees in cities and states that require employers to provide some form of commuter benefit, you may be required to continue to facilitate transportation fringe benefits; consider the potential additional cost of compliance.

- When a final law is passed, contact the Executive Compensation and Benefits Team at Pillsbury for guidance on how to comply with the changes.

For a summary of changes contemplated by the House Bill and the Senate Proposal that relate to executive and equity compensation, see our alert “Tax Reform: The Shifting Landscape of Executive and Equity Compensation.”