Alert

Tax Reform: The Shifting Landscape of Executive and Equity Compensation

The House and Senate propose wide-sweeping amendments to the tax rules regarding executive and equity compensation that would affect public and private for-profit companies as well as tax-exempt organizations.

Alert

By

Takeaways

11.17.17

Tax reform, including changes to the taxation of executive compensation, is on the horizon as both the House and Senate move forward with legislative efforts. On November 16, 2017, the House passed its tax reform bill, the Tax Cuts and Jobs Act. The Senate released its own proposal on November 9, 2017 which was significantly changed by the Chairman’s mark on November 14, 2017 and was approved with amendments on November 16, 2017. Over the past weeks, the House Bill and the Senate Proposal have become gradually aligned with respect to executive and equity compensation; however, significant differences remain.

Background

On November 2, 2017, the House of Representatives introduced its “Tax Cuts and Jobs Act,” a tax reform bill that proposed to dramatically alter the tax treatment of executive and equity compensation. Before the ink was dry, on November 6, 2017, the Chairman of the House Ways and Means Committee, Kevin Brady, released amendments that scaled back some of the more far-reaching amendments proposed by the initial House bill. The House Ways and Means Committee approved the amendments on November 9, 2017 and sent the revised bill (the “House Bill”) to the full House for a vote. The House passed its bill on November 16, 2017.

Amidst the commotion, on November 9, 2017, the Senate Finance Committee released its own tax reform proposal, “Description of the Chairman’s Mark of the ‘Tax Cuts and Jobs Act.’” The mark-up process of the proposal lasted nearly a week and, on November 15, 2017, the Senate Finance Committee released its current proposal (the “Senate Proposal”) which also eliminated certain wide-sweeping amendments included in the initial Senate tax reform proposal. The Senate Finance Committee approved its current proposal with minor additional developments late on November 16, 2017.

Both the House Bill and the Senate Proposal are anticipated to evolve as they move through the legislative process. The House Bill and the Senate Proposal have become increasingly aligned, although the table below reflects that key differences remain. If the Senate’s Proposal is passed as it currently stands, it is anticipated that the differences would be reconciled in Conference.

The Proposed Laws

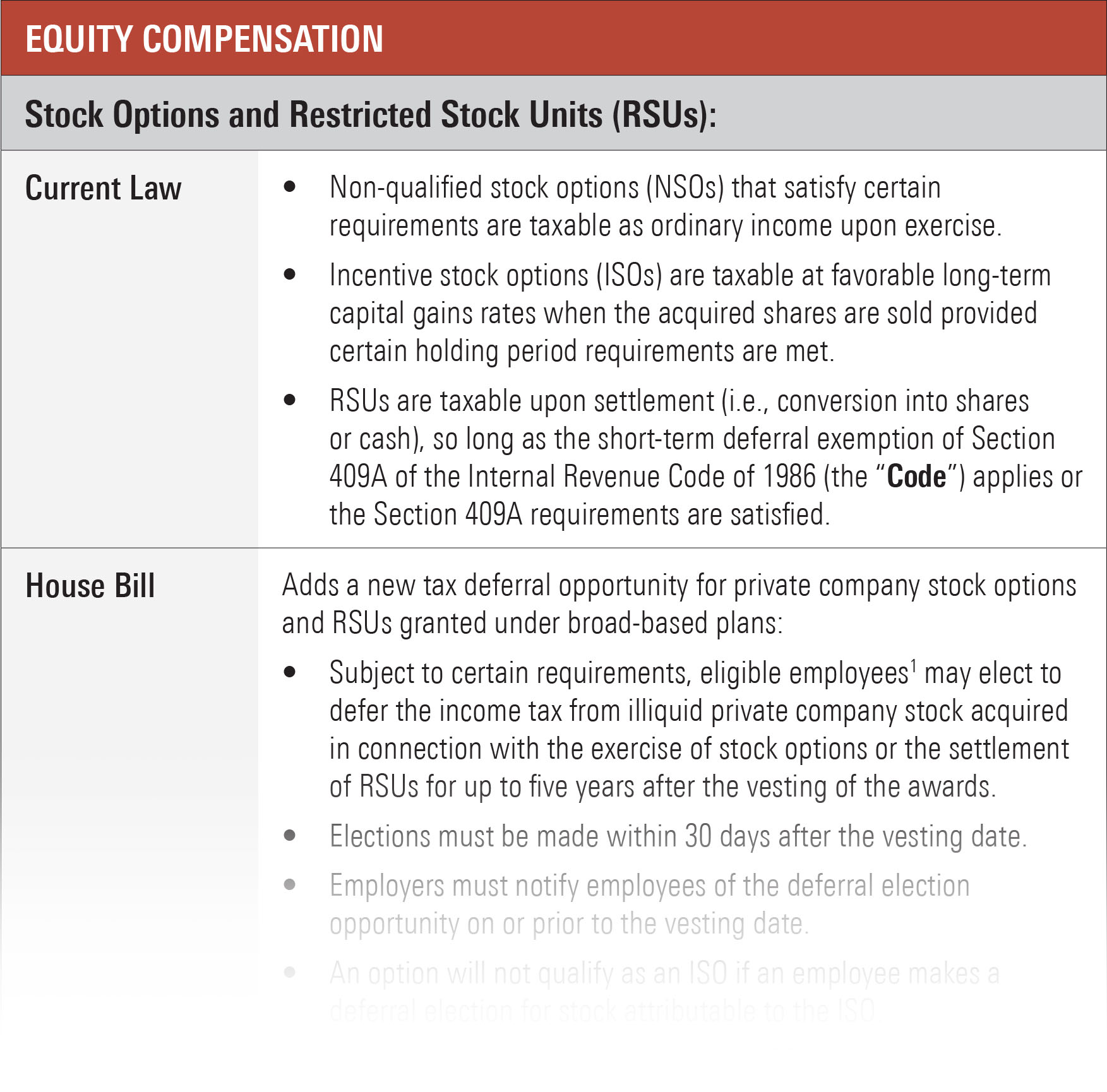

The table below summarizes key executive and equity compensation provisions of the House Bill and the Senate Proposal.

Click here to view the full table (pdf).

Practical Considerations

It is essential that employers continue to closely monitor progress on Congress’s tax reform effort, be educated and be prepared to respond to changes as they arise. The bill adopted by the House and amendments proposed by the Senate reflect significant changes over the past two weeks and we expect that they will continue to do so as we approach year-end. That being said, Republican Party leaders controlling the House and the Senate have expressed a strong desire for enactment of reforms within a matter of weeks. When a final law is passed, please contact the Executive Compensation team at Pillsbury for guidance on how to comply with the new tax law and take advantage of new planning opportunities.

For a summary of changes contemplated by the House Bill and the Senate Proposal to the taxation of employee benefits, see our alert “A Moving Target: Tax-Qualified Plans and Other Employee Benefits.”