Alert 07.03.25

Alert

Treasury and IRS Issue Proposed Regulations Under IRC Section 45Z Clean Fuel Production Credit

Alert

By Don Lonczak, Steve R. Brenner, Baylee Beeman, Jason Drogin Atwood

Takeaways

03.06.26

Recently, the U.S. Department of the Treasury (Treasury) and the Internal Revenue Service (IRS) released long-awaited proposed regulations (the Proposed Regulations) under Section 45Z of the Internal Revenue Code of 1986, as amended (IRC), providing comprehensive guidance on the clean fuel production credit (CFPC) enacted by the Inflation Reduction Act of 2022 and amended by the One, Big, Beautiful Bill Act of 2025 (OBBBA). The Proposed Regulations largely follow the approach taken in last year’s draft form of proposed regulations (Draft Regulations) that was included as part of IRS Notice 2025-10. As discussed below, however, the Proposed Regulations include several significant modifications from the Draft Regulations in response to comments submitted to Treasury and amendments to IRC Section 45Z made by the OBBBA.

Written comments, requests to speak and outlines of speaking topics relating to the Proposed Regulations are due by April 6, 2026, and a public hearing will be held on May 28, 2026, at 10:00 am ET.

Brief Overview of the IRC Section 45Z

IRC Section 45Z provides a tax credit, the CFPC, for qualifying clean transportation fuel produced in the United States after December 31, 2024, and sold by December 31, 2029. The CFPC replaces a mix of prior income tax credits and excise tax credits for biodiesel, renewable diesel, alternative fuels and sustainable aviation fuel (SAF). To qualify, a taxpayer must (i) produce a qualifying transportation fuel at a qualified facility located in the United States; (ii) register as a producer under Section 4101 of the Code by the time of the production; (iii) meet life cycle greenhouse gas (GHG) emissions thresholds; and (iv) sell the fuel to an unrelated person in a qualified sale during the taxable year.

The CFPC is calculated by multiplying the applicable per-gallon (or gallon-equivalent) amount by the volume of fuel sold in a qualified sale, and the fuel’s emissions factor. The fuel emissions factor measures the reduction in life cycle GHG emissions relative to a statutory baseline of 50 kg CO2e per mmBTU. For non-SAF transportation fuel, the base rate applicable amount is $0.20 per gallon (or gallon equivalent), increasing to $1.00 if prevailing wage and apprenticeship requirements are satisfied. The same base and increased rates apply to SAF produced after December 31, 2025, but prior to amendment by the OBBBA, SAF was eligible for a base rate of $0.35 per gallon (or gallon equivalent), or an increased rate of $1.75 per gallon (or gallon equivalent) assuming compliance with the prevailing wage and apprenticeship requirements.

Emissions rates for transportation fuel generally are intended to be based on an annual emissions rate table to be published each year by the IRS. The first annual emissions rate table was released on January 10, 2025, and producers are awaiting an updated table for 2026. In cases where the annual emissions rate table does not reflect a particular transportation fuel, IRC Section 45Z contemplates the possibility for producers to petition Treasury for a provisional emissions rate (PER) determination.

Highlights of the Proposed Regulations

Qualified Sales

In order to claim the CFPC, a producer must sell transportation fuel to an unrelated person: (i) for use in the production of a fuel mixture; (ii) for use in a trade or business or (iii) for resale at retail by placement in the fuel tank of another person (a Qualified Sale). Significantly, in a departure from the Draft Regulations, the Proposed Regulations make clear that “use in a trade or business” does not require the use to be as a transportation fuel. Furthermore, the Proposed Regulations expressly state that a sale for use in a trade or business includes a sale of fuel to an unrelated person who subsequently resells the fuel in its trade or business. These significant clarifications should eliminate concerns that sales to a third-party marketer or other intermediary would not be considered Qualified Sales for purposes of IRC Section 45Z as long as re-sale activities represent part of the trade or business of the relevant marketer or intermediary.

Prior to amendment by the OBBBA, IRC Section 45Z provided limited relief for sales of transportation fuel to related persons, allowing only sales between members of a consolidated group of corporations to be considered Qualified Sales in situations where the purchasing member subsequently sells the fuel to an unrelated person. The OBBBA, however, provided a broad grant of regulatory authority for Treasury to prescribe additional exceptions to the related person restriction. Based on such regulatory grant of regulatory authority, the Proposed Regulations now would allow a sale of transportation fuel to any “related person” to constitute a Qualified Sale if the related person re-sells the fuel to an unrelated person.

A “related person” for purposes of the expanded relief provided by the Proposed Regulations is defined by reference to the “single employer” rules under IRC section 52(b). Very generally, under such rules, a related person would include any form of organization, including a partnership or sole proprietorship, conducting a trade or business that controls, is controlled by or is under common control with, the seller of transportation fuel, using a greater-than-50% ownership standard. From a timing perspective, when transportation fuel is sold to such a related person, a Qualified Sale does not occur until the related person completes the re-sale transaction to an unrelated person.

Producer/Production

As defined in the Proposed Regulations, the producer is the person that engages in the production of transportation fuel. A producer is not required to own the production facility, and multiple producers may use the same facility. The production activity includes all steps and processes used to make transportation fuel, starting with the processing of primary feedstocks and ending with transportation fuel that is ready to be sold. Blending, however, is not considered a production activity, even if the resulting fuel mixture meets the requirements for a transportation fuel under IRC Section 45Z, essentially because a production activity must include substantial processing and a chemical transformation. Treasury and the IRS noted in the Preamble to the Proposed Regulations that the enactment of IRC Section 45Z as a producer credit, coupled with the expiration of the prior blender credits, signaled congressional intent to end tax incentives for blending activities.

Fuel/Transportation Fuel

The term “fuel” is defined in the Proposed Regulations as any liquid or gaseous substances that can be consumed to supply heat or power. Notably, electricity is not considered a fuel. The preamble to the Proposed Regulations points to the availability of different clean energy credits for electricity production under IRC sections 45Y and 48E, among other factors, to justify the exclusion of electricity.

The Proposed Regulations modify the statutory definition of “transportation fuel” to include a requirement that the fuel cannot be produced from a fuel for which a [CFPC] is allowable. The newly added final requirement is intended to address situations where the primary feedstock used in the fuel production process already is a qualifying transportation fuel in order to avoid the possibility of double-counting of the CFPC. Also, the Proposed Regulations make clear that actual use in a highway vehicle or aircraft is not required in order to constitute a transportation fuel. Instead, a fuel meets the suitable for use requirement if it has practical and commercial fitness for use in a highway vehicle or aircraft, or may be blended into a mixture with the requisite practical and commercial fitness for such use.

Gallon Equivalent for Non-Liquid Fuels

The Proposed Regulations provide guidance with respect to the determination of the “gallon equivalent” of non-liquid fuels, which includes fuels “in a gaseous state at ambient pressure and temperature of 1 atmosphere and 60 degrees Fahrenheit, respectively.” Commenters had expressed interest in having gallon equivalence tied to ethanol so as to allow for increased credit amounts. Despite such requests, Treasury and the IRS decided that gasoline was the best measure of energy equivalence given that (i) gasoline remains the most common transportation fuel in the United States and (ii) IRC Section 45Z was enacted to incentivize alternatives to fossil fuels.

Key OBBBA Changes Reflected in the Proposed Regulations

The Proposed Regulations reflect several significant amendments made by the OBBBA.

Based on amendments under the OBBBA, the Proposed Regulations provide that the determination of emissions rates for fuels produced after December 31, 2025, does not take into account emissions attributable to indirect land use change. Additionally, in accordance with the OBBBA, the Proposed Regulations state that the emissions rate for fuels produced after December 31, 2025, cannot have a negative value, with the exception of fuels produced from a primary feedstock of animal manure. The legislative change eliminates the possibility that the CFPC rate could be greater than the statutory rate of $1.00 per gallon (assuming prevailing wage and apprenticeship requirements are met) for transportation fuels that have emissions rates below zero. As to the exception for animal manure feedstocks, the OBBBA granted Treasury regulatory authority to allow for such an exception, and the Proposed Regulations suggest that Treasury will do so.

The Proposed Regulations also adopt the OBBBA changes related to foreign feedstocks and prohibited foreign entities. Thus, consistent with the OBBBA, transportation fuel produced after December 31, 2025, must be exclusively derived from feedstocks obtained in the United States, Canada or Mexico. Additionally, the CFPC is unavailable for taxable years beginning after July 4, 2025, for taxpayers that are “specified foreign entities” and for taxable years beginning after July 4, 2027, for taxpayers that are “foreign influenced entities.” Very generally, under IRC section 7701(a)(51), a specified foreign entity is one that has significant ownership by persons in “covered nations” (namely, China, Russia, Iran and North Korea), and a foreign influenced entity is one that, by contract or otherwise, allows persons in covered nations to influence certain major decisions.

Determination of Emissions Rates/PER Petitions

The emissions rate for a transportation fuel is determined either by using the annual emissions rate table issued by Treasury and the IRS (most recently in IRS Notice 2025-11), or if the table does not establish an emissions rate for a particular fuel, by application for a PER. An emissions rate table is considered to establish the emissions rate for a fuel only if the table includes both the type and category of fuel, and the Proposed Regulations make clear that the PER petition process is available only where the applicable emissions rate table does not establish an emissions rate for the producer’s type and category of fuel. Where a transportation fuel is included in the table, the producer must use the table and is not eligible to seek a PER.

As general matter, the most recent 45ZCF-GREET model released by the U.S. Department of Energy (DOE) that reflects the relevant fuel will be the only allowed methodology for determining life cycle greenhouse gas emissions for non-SAF transportation fuels, with either the 45ZCF-GREET model or a CORSIA methodology allowed for SAF. The model is designed to support consistent, comparable and administrable emissions determinations across taxpayers and therefore relies on a combination of facility-specific operational inputs and standardized background assumptions that cannot be modified. As a result, the extent to which taxpayers can reflect highly granular or facility-specific operational characteristics in their emissions calculations may be constrained by the model’s structure.

The Proposed Regulations provide various requirements for obtaining PERs. Before filing a PER petition, a taxpayer first submits a request to the DOE for an emissions value for an eligible fuel, and then must await receipt of a “calculated emissions value letter” (CEVL) from the DOE for such fuel. Thereafter, the taxpayer can submit a PER petition in accordance with the procedures set forth in the Proposed Regulations (and any petition that does not follow such procedures will be automatically denied). The PER petition, which would include the CEVL, would be filed with the taxpayer’s tax return for the first taxable year in which CFPCs are claimed for the fuel to which the petition relates. A properly filed PER petition will be deemed accepted by the IRS such that the taxpayer can rely on the EV established by the DOE until such time as an emissions rate for the relevant fuel is established in an annual emissions table.

Registration, Record-Keeping and Substantiation

In order to claim the CFPC, a taxpayer must be registered as a producer of clean fuel in accordance with IRC Section 4101. Registration must be in place at the time of production, and the CFPC will not be available if registration been finalized. The Proposed Regulations also include three tests that must be satisfied in order to obtain the required letter of registration to claim the CFPC: (i) an activity test that looks to whether the taxpayer is regularly involved in the production of transportation fuel in the course of its trade or business, (ii) an “acceptable risk” test that focuses on potential wrongful acts by the taxpayer and (iii) a tax history test based on the taxpayer’s compliance with federal tax laws.

Detailed requirements are provided in the Proposed Regulations as to the documentation that taxpayers are required to maintain in order to support claims for the CFPC, including information with respect to primary feedstocks, determinations of emissions rates and establishing that Qualified Sales occurred. Here, the Proposed Regulations provide some helpful safe harbors to substantiate CFPC claims. With respect to substantiation of emissions rates, a taxpayer may comply with the certification procedures applicable to SAF production, which generally would require verification by a qualified, independent party. As to demonstrating Qualified Sales, the Proposed Regulations allow for certifications to be obtained by the third-party purchasers of the transportation fuel and for this purpose a form of model certificate is provided that can be used by taxpayers.

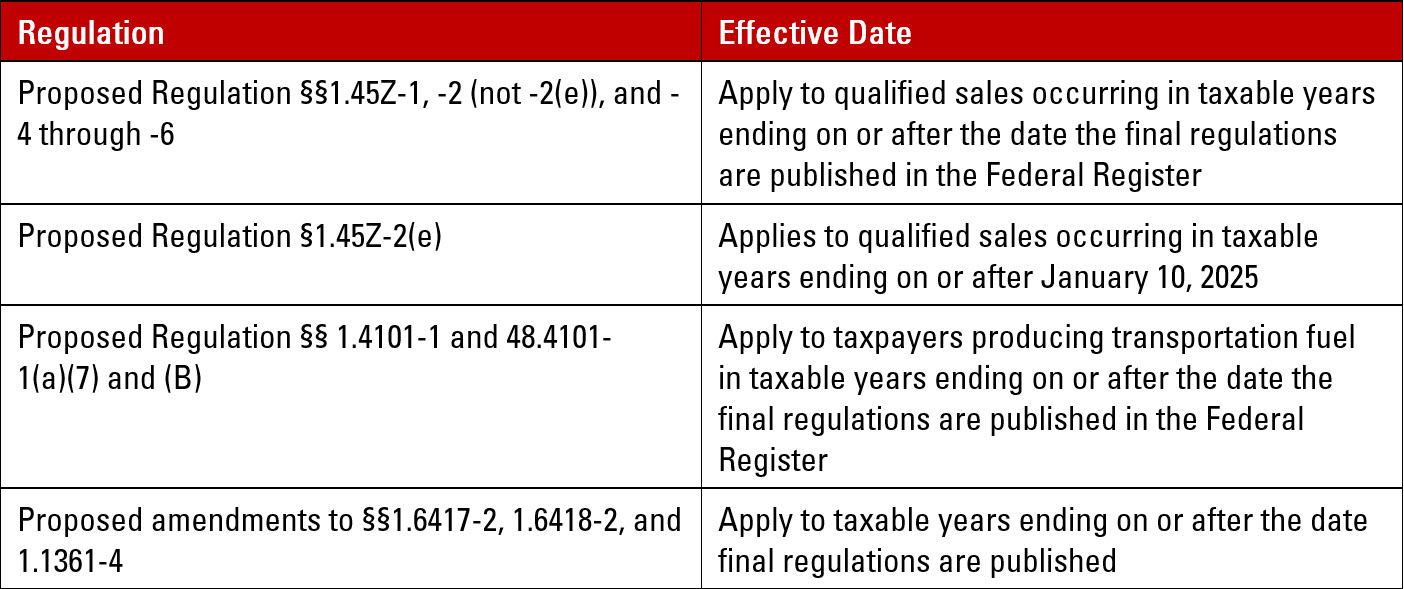

Effective Dates

The Proposed Regulations include multiple applicability dates, summarized below. Taxpayers may rely on the Proposed Regulations prior to finalization, provided the rules are applied in their entirety and in a consistent manner.

Final Thoughts

The Proposed Regulations provide long-needed clarity on IRC Section 45Z, particularly with respect to Qualified Sales and end-use of transportation fuel. Additionally, the procedures provided for obtaining PERs will allow producers using new feedstocks or methods of fuel production to obtain comfort on the availability of CFPC. Taxpayers producing or investing in clean transportation fuels should carefully evaluate their production arrangements, sales channels and registration posture in light of the guidance offered by the Proposed Regulations. Please reach out to any of our Pillsbury team members to discuss the impact of the Proposed Regulations on your on-going and/or future projects.

These and any accompanying materials are not legal advice, are not a complete summary of the subject matter, and are subject to the terms of use found at: https://www.pillsburylaw.com/en/terms-of-use.html. We recommend that you obtain separate legal advice.